.png?width=1000&height=1000&name=Market%20Report%20FR%20main%20visual%20(1).png "Market Report FR main visual (1)")

Local EV Penetration down to the Road Segment

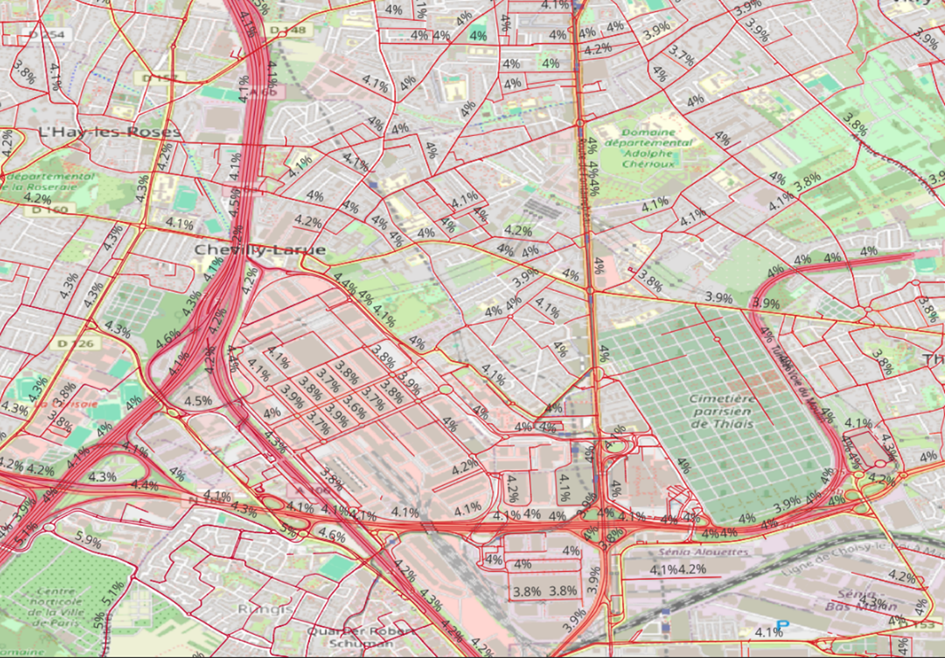

France’s EV transition does not only differ by region or department. It also varies street by street. When looking at EV penetration at the road-segment level, clear patterns appear across cities and suburbs.

This level of detail helps operators understand where demand is forming in real time. It highlights where fast charging will soon be needed, where AC coverage can support daily routines, and where gaps remain in neighborhoods that appear similar at a larger scale.

How can you create your most profitable network by 2030?

In the sprint towards the 2030 targets, making smart, data-driven location decisions is more critical than ever. Acting quickly is essential, but acting strategically is what drives real returns. True ROI comes from placing the right type and number of charging points at locations where connection costs are viable and demand is proven.

To do this effectively, you need clear insights into the factors that define the performance of EV charging stations: from car passage and dwell time to local activity and infrastructure access. But gathering, combining, and analyzing all that data? That’s a challenge.

That's where ChargePlanner comes in. The platform lets you simulate and test multiple configurations at once, combining best-in-class market data, local visitor behavior, and predictive AI.